The Great Interest Reset: Trump’s Strategy to Save the US from Biden’s Borrowing Binge

The national debt has become something of a metaphysical object in American politics: omnipresent, quietly oppressive, and strangely intangible. One cannot touch it, but one can certainly feel its weight. Like a fog over the fiscal landscape, it obscures clarity and threatens disaster. And yet, we muddle through. We borrow, we spend, we shrug. Until now.

What President Trump understands—with a clarity that escapes both Keynesian academics and the Biden Treasury—is that debt is not merely a numerical sum but a dynamic instrument, subject to manipulation by policy, psychology, and sovereignty. The question, then, is not whether the United States can "afford" its debt, but whether it can govern the terms under which that debt is managed, rolled over, and refinanced.

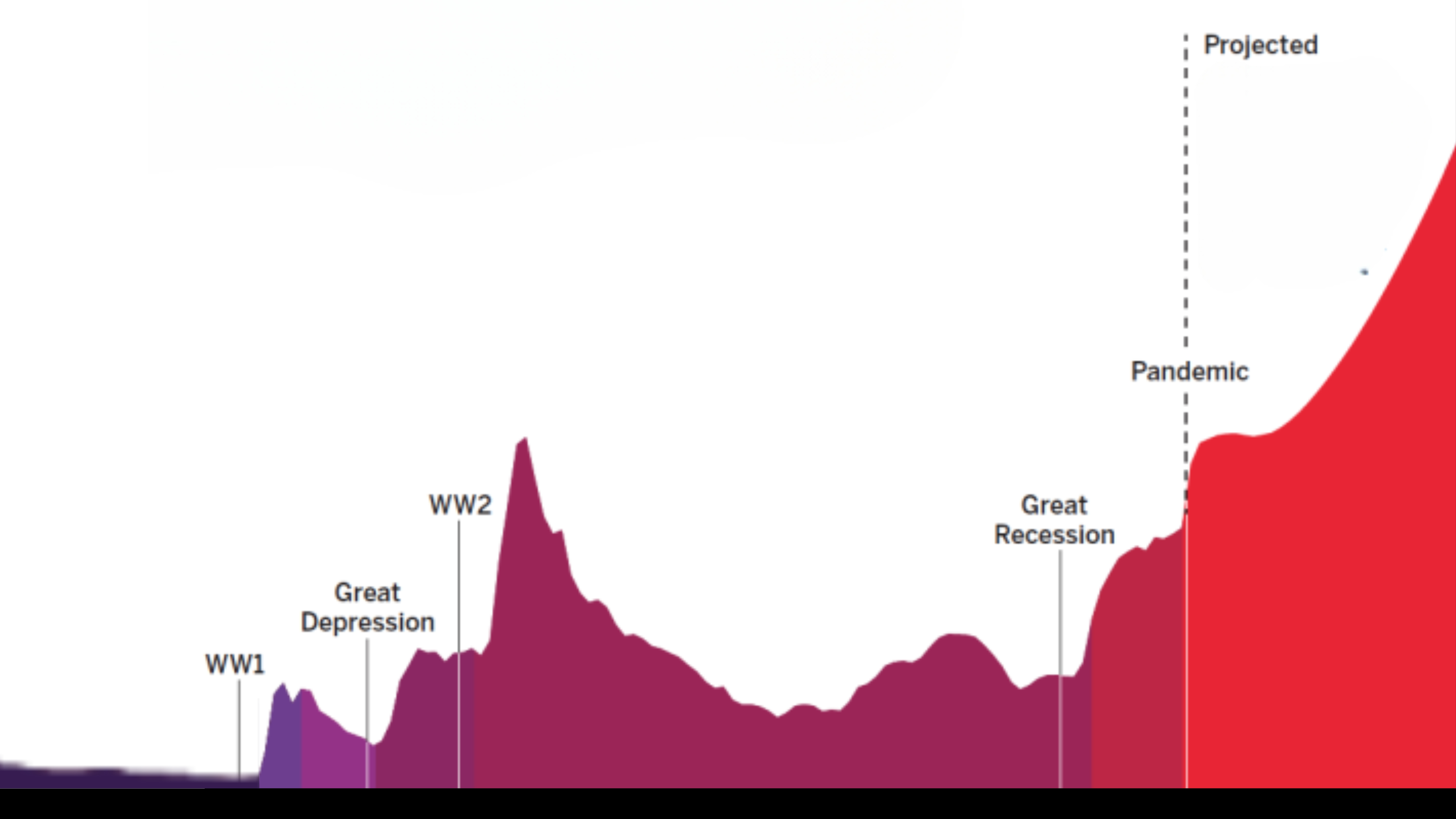

This is not a hypothetical concern. As of March 2025, the United States holds $36.22 trillion in gross national debt, of which $28.9 trillion is held by the public. Critically, a full one-third of that publicly held debt—some $9 trillion—will mature within the next 12 months. This is not merely a fiscal inconvenience; it is a crisis of arithmetic. Bonds do not self-renew. We must go back to the markets, hat in hand, to replace those maturing notes. The question is: at what price?

Herein lies the genius—yes, the genius—of Trump's fiscal maneuvering. Where his predecessor saddled the Treasury with trillions in three- and five-year bonds at rates now proven shortsighted, Trump sees the trap for what it is: a forced refinancing at higher rates, a compounding burden that transforms debt from a tool of leverage into a runaway liability.

The average interest rate on U.S. debt five years ago was 2.32%. Today, thanks to Biden-era borrowing, it stands at 3.35%. That 1.03 percentage point increase may seem minor until one considers scale: it represents a 44% rise in the cost of borrowing across the entire debt portfolio. In dollar terms, the interest payments alone now rival, and will soon exceed, the entire Pentagon budget. Interest is no longer a budget line item. It is the budget.

Trump's solution is threefold: reduce federal outlays by slashing fraud, waste, and bureaucratic inertia; pressure foreign governments to reduce tariffs and thus open new markets for American goods; and attract an unprecedented influx of foreign capital—$3 trillion and counting—into U.S. assets, infrastructure, and enterprise.

Each prong of this strategy is essential to bending the yield curve downward, thereby reducing the effective rate at which new debt is issued. Let us examine them in turn.

First, spending. Elon Musk, now at the helm of the Department of Government Efficiency (DOGE), is not merely cutting fat—he is torching it. From duplicative grants to misallocated welfare programs to climate consultancy boondoggles, the administration is moving with surgical speed. Every dollar cut from projected outlays lowers expected deficits. Lower deficits mean less upward pressure on yields. Less pressure, lower rates.

Second, trade. Tariffs are not, contrary to mainstream myth, mere taxes on consumers. When deployed strategically, they are bargaining chips. Trump wields them as such. By threatening retaliatory tariffs or selective decoupling, he compels trading partners to reduce their own barriers, which in turn boosts American exports. Exports are taxable. More exports, more revenue. More revenue, less need to borrow.

Third, investment. The arrival of trillions in foreign capital into the American economy—whether in the form of equity stakes, real estate purchases, or industrial buildouts—is not a coincidence. It is a vote of confidence. Capital goes where it is treated best. Under Trump, capital finds low regulatory drag, high expected returns, and a government openly courting investment. Foreign demand for U.S. assets bolsters demand for the dollar, for Treasuries, and for long-term American stability. Demand for Treasuries with a strong bid-to-cover ratio allows issuance at lower rates. And again, lower rates mean less interest expense.

To fully appreciate the risk and reward of Trump’s economic gambit, one must understand the broader context. This is a high-stakes plan, intentionally structured to reverse the long-term erosion brought on by NAFTA and globalization. By implementing reciprocal tariffs, Trump is applying strategic pressure to restore equilibrium to trade relationships. The outcome remains uncertain; it is neither a guaranteed disaster nor an assured success.

Consider the price of commodities. They are falling, and the decline is expected to continue. Whether tariffs will adequately compensate for that deflationary pressure is unclear. In the short term, falling oil and real estate prices may bring welcome relief to consumers, lowering living costs and undermining the inflation panic of the last three years. But there is a catch: asset deflation could expose the fragility of the post-COVID paper millionaire class, whose perceived wealth was tied to inflated valuations rather than productive output.

Take housing. The average home now costs $419,000, financed at interest rates near 7%. This is not a sustainable condition for a healthy middle class. If prices fall, the pain may be acute—but necessary. Just as false idols must be shattered, so too must the illusion of prosperity built on inflated credit.

Even if inflation retreats and purchasing power improves, the reconstruction of a stable, dignified working-class economy will not be instantaneous. It is a long-term effort. Decades of offshoring, demoralization, and cultural decay cannot be repaired in a fiscal quarter. They demand time, patience, and institutions beyond government—especially churches and civic associations—to restore the moral foundation.

The stock market, meanwhile, should not be treated as a sacred totem whose line must always ascend. The idea that equities should rise perpetually is a modern pathology fueled by deficit spending and monetary manipulation. Historically, markets had bad years. What changed is not economic reality but the refusal to accept it. Trump’s plan dares to reset expectations.

And the fiscal picture is undeniably unsustainable. Federal deficits exceeding 4 to 5% of GDP are not signs of temporary strain; they are red flags of structural imbalance. In 2021, a reckoning was postponed by massive infusions of federal cash. But that postponement has only intensified the coming correction.

No one knows the precise timeline for this reckoning. It could erupt in weeks or linger for years. But structural change is underway, and it will not be easy. Trump’s plan recognizes this truth and acts accordingly.

A skeptic might ask: isn’t Trump simply inflating a different bubble? What if investment slows? What if tariffs provoke retaliation? What if spending cuts are blocked by Congress? These are fair questions. But they are also loaded with an asymmetry of scrutiny. Under Biden, $1.78 trillion was added to the national debt in just the past year, and few within the cathedral of respectable economic opinion batted an eye. Under Trump, the mere attempt to reverse course provokes howls of protest.

Even so, the risk calculus is not symmetrical. Rolling $9 trillion in debt at 5% would cost $450 billion annually. Rolling it at 3% saves $180 billion per year. Over a decade, that difference is $1.8 trillion—a number equal to Biden's entire 2024 deficit. The stakes are not small.

To those who doubt the feasibility of Trump’s strategy, I offer the following thought experiment. Suppose the United States could credibly signal to bond markets that it would balance the budget within a decade. Suppose further that it could demonstrate sufficient political will to suppress inflation, protect capital, and spur growth. In such a world, why would the yield on Treasuries not fall? Why would investors not bid more aggressively on U.S. debt, driving rates down?

Indeed, this is what happened in the late 1990s under the Clinton-Gingrich fiscal détente. Yields fell, markets rose, and for a brief moment, the U.S. ran surpluses. The difference now is that Trump is not merely hoping for budget discipline. He is engineering it.

Beneath all of this lies a deeper philosophical point. Debt, properly understood, is a bet on the future. It presumes that tomorrow will be richer than today, and that the marginal utility of today’s dollar is greater than tomorrow’s repayment obligation. But when debt is used to fund inefficiency, decadence, or ideological crusades, it ceases to be an investment. It becomes a liability to be managed, not a resource to be allocated.

Trump understands this. That is why his fiscal strategy is not merely about cutting costs, but about restoring discipline. The goal is not austerity for its own sake. It is sovereignty—the freedom to choose how we finance our future, rather than be beholden to creditors, foreign central banks, or the whims of interest rates set by the market.

Critics deride Trump’s approach as chaotic. But chaos, in this context, is a euphemism for disruption. Disruption of the status quo. Disruption of the fiscal sleepwalk that has characterized the post-COVID period. And disruption, as any entrepreneur will tell you, is the necessary prelude to renewal.

Let us then not dismiss Trump’s debt strategy as a series of disconnected stunts. It is a coherent, integrated plan to realign America’s fiscal posture with its founding values: prudence, independence, and strength. If it succeeds, the United States may yet reassert control over its financial destiny. If it fails, it will not be for lack of clarity, coherence, or conviction.

Trump is not merely trying to make America great again. He is trying to make its balance sheet sane again. And that, in the shadow of $36 trillion in debt, may prove the greater miracle.

If you don't already please follow @amuse on 𝕏.

Thankyou sir. Spoken in words I understand. It is a gamble, but it is one we can't afford to lose. Thank the Lord we have President Trump and an assemblage of top notch financial advisors to see us through

Superb!! Really superb! You have helped us make sense of national debt and tariffs. Thank you!